BAC: Bank of America Stock Research

BAC: Bank of America Stock Research

Updated 3/9/2022

Don’t understand some business words here? Open the FAQ in another tab.

Summary of Operations

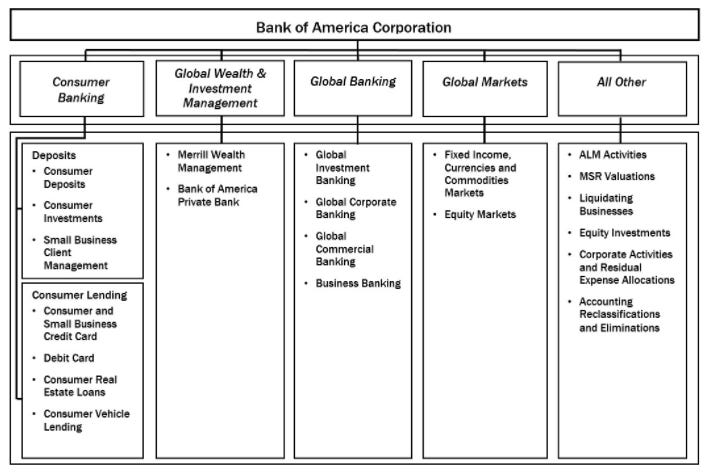

Bank of America (BoA) is one of the largest banks and financial institutions in the world, the product of several mergers and acquisitions over decades. It classifies its operations into four segments:

Consumer Banking

Global Wealth & Investment Management (GWIM)

Global Banking and Global Markets

All Other

The vast majority of its business occurs in the United States. As of 2021, BoA had 67 million consumer accounts, 41 million active users on its website, 4,200 locations, and 16,000 ATMs. About half of its income derives from interest earned on loans, the other half being noninterest income (including unrealized capital gains). Much of this derives from a variety of fees it charges for its services.

In 2021, BoA reported over $30 billion in net income and over $3 trillion in assets.

Strategy

After the disaster of the 2008 Financial Crisis, BoA has followed a policy of “responsible growth” under its CEO Brian Moynihan. It maintains sufficient cash to cover its debts and is much more frugal in its dividend payouts. BoA competes with its recognizable brand, enjoying synergies with its investment wing (Merrill Lynch), and proving quality service to its customers. With its size, customers enjoy accessibility wherever they may be in the United States, and its Web services improve on this advantage.

Growth and the Future

Its cautious, more “slow and steady” approach, combined with its large size, make BoA a slow grower but at little risk of downside. Nicknamed “Buffett’s favorite bank,” Berkshire Hathaway possesses a major position in it, most of which came from convertible preferred shares that it offered in 2011. If its responsible growth model doesn’t protect it from all headwinds, I believe BoA has a friend in Berkshire to recapitalize it, which should ease the minds of those who are long on shares of BAC.

The growth of the bank should track with GDP growth, as well as its ability to acquire and retain new accounts. Buybacks will also create value for the long-term holder. About $25 billion was spent in 2021 for buybacks, increasing the holder’s position 7%.

We cannot forget the dividend either. BAC paid $0.78 per share in 2021, up 8.3% from the year before, with a streak of increases many years before that.

Valuation

Growth Assumptions: 10%

Intrinsic Value Per Share: $30

Done reading this article? Return to the main library.