FRG: Deep Dive

Don’t understand some business words here? Open the FAQ in another tab.

Description of Business

Franchise Group, Inc. (FRG) is a holding company that acquires and owns franchised and franchisable businesses. “Franchisable” means the corporate stores can be converted to franchised stores, where a franchisee buys the store but continues to operate under that brand, while the franchise is entitled to a cut of the store’s sales.

It seeks assets with high operating margins and aims to cover diverse sectors in order to provide reliable cash flows to FRG as a whole. These acquisitions have historically been made with its own cash generation, debt financing, and the sale of new shares. Long term, cash is generated for FRG through its cut of the franchise’s revenues, while the capex is mostly outsourced to the franchisees that operate individual locations.

The company hopes to provide a growing dividend to shareholders. Thus, the dividend might be understood to be the concentrated income derived from each of the portfolio’s franchises, passed onto the shareholder. Let’s take a look at those franchises.

Key Assets

The company’s portfolio currently consists of these six companies.

The Vitamin Shoppe

Sells vitamins and other supplements across most of the U.S. Currently it sells third-party merchandise, but it’s switching to its own private labels, in order to fatten its margins.

American Freight

Retailer of low-cost furniture and appliances. Covers much of the U.S. but has room to saturate regions more thoroughly.

Pet Supplies Plus

A leading retailer of pet products, growth lies in the conversion of stores that are still corporate-owned and expansion into other regions.

Buddy’s

Works the in the Rent-To-Own business (goods are rented by customers with an open option to buy). Most of these stores are already franchised, but these conversions have provided a solid blueprint for FRG’s future acquisitions. It primarily operates in the South, providing room for organic growth nationwide with minimal capex from FRG.

Sylvan Learning

This is a private tutoring company that provides services ranging from preschool to high school. Nearly all of these are franchised, so organic growth into the tutoring market is where its future lies. The extent of its tutoring services means that it could acquire long-term customer accounts.

Badcock

Deals in a variety of home furnishings. Only a fraction are still corporate owned, but being concentrated in the Southeast, there is room for more growth across the country.

History of the Company

The tale of FRG is, in many ways, the tale of its founder, chairman, and CEO: Brian R. Kahn. Kahn founded Vintage Capital in 1998 (originally known as Kahn Capital). To date, this company owns about 12% of FRG, and Kahn personally owns about 30% of the shares. Thus, he has a substantial interest in FRG’s success.

The first seeds are when Vintage acquired Liberty Tax in 2018. Formally, FRG came into being in 2019, wherein Liberty Tax merged with Buddy’s. From there, the company has taken to its new identity as a conglomerate and seeks acquisitions at a reasonable price. For example, Liberty Tax was acquired for $160 million and sold for $240 million three years later (while generating cash in the meantime).

Overall, the history of FRG is short since it only goes back a few years. The diagram above neatly outlines the timeline of its acquisitions.

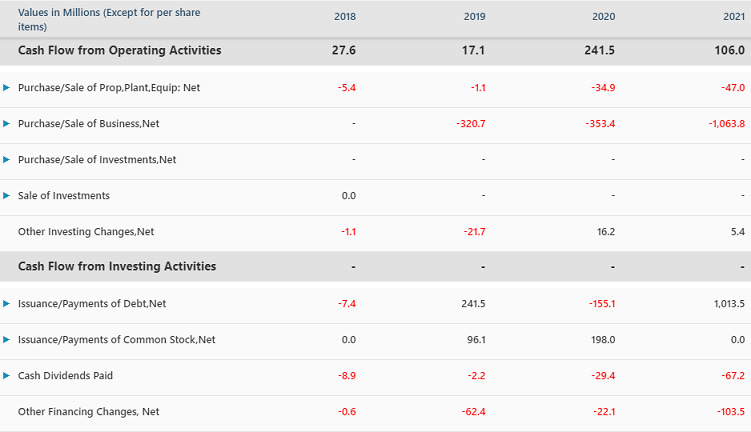

Financials

As we can see below, the company’s operating cash flows have increased significantly, following their acquisitions. We also see that these purchases have variably been financed by debt, new shares, and cash on hand, while also still committing cash to its dividend.

Big Debt?

The current strategy is to rely more on debt than the sale of new shares, in order to protect current owners from dilution. As of the year ended 2021, the company had $1.9 billion in debt, which is close to its usual market cap. Normally this is cause for alarm, but FRG has a plan. While debt is often called “leverage” euphemistically, the real advantage that FRG leverages is its franchising model. By the end of Q1 2022, they had used this to reduce the debt down to $1.3 billion.

Specifics will help. Badcock’s acquisition is a reason for much of the debt on balance. By selling off real estate assets that are unneeded, FRG generated cash (and has other deals that are about to close) to reduce their debt. More commonly, FRG receives cash when it franchises its corporate-owned stores, further assisting in paying off the debt that was taken on to acquire those stores, while still deriving income from the franchise operation.

The wheel of repayment spins smoothly. Because the franchise model allows for easy liquidation of unneeded assets and continued cash generation, FRG can repay its debt, improve its credit, and thus open the door to larger loans for further acquisitions. This will probably prove to be their secret sauce in the long run.

Management Team

I already talked a bit about Kahn. Let’s highlight another interesting member of the management team.

Todd Evans

He is the Chief Franchising Officer. A good interview with him can be found here. He has a breadth of experience in franchise operations and understands them at a fundamental level, which explains why FRG has this repeatable model.

Intrinsic Value

Dividend

Because the dividend is a key part of the concept for this stock (and the yield is near 7%), some people might value the stock on that alone. Assuming a 20% growth rate, the dividend makes this stock worth about $64.

Cash Flows

If we focus on the overall cash flows, starting from 2021 FCF of $60 million, with the same 20% growth rate, that makes the a fair value of the stock about $36.

Book value is about $19 as well.