FROG: Jfrog Stock Research

Updated 3/30/2022

Don’t understand some business words here? Open the FAQ in another tab.

Summary of Operations

Jfrog is an interesting company, describing itself as part of the “DevOps” industry. It’s not easy to put this company’s operations into simple words. It has a platform, the Artifactory, that essentially allows businesses to centralize and synchronize their software needs across the company, for a variety of benefits. Thankfully, they made a video on their YouTube that helps to visualize it. It’s only two minutes, so I suggest watching it.

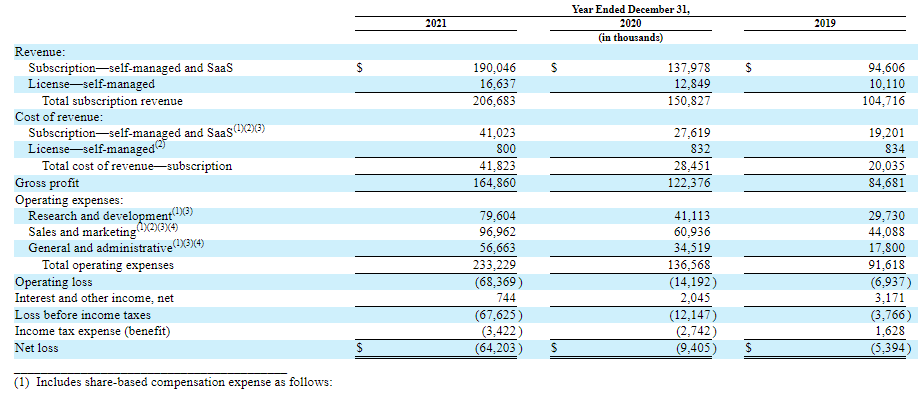

Their customers are diffuse, and their 10 largest only account for about 7% of revenues. Nearly all revenues come from subscriptions.

While they reported a loss, much of this is due to share-based compensation. Operating cash flows are consistently positive.

Strategy

They acquire customers with a flexible product, allowing free-trials and tiered subscriptions to suit customers’ needs. With investments in their inbound sales team and improvements in their technology and features, they aim expand on their current accounts and grow with new accounts, new features, and expansion in a global market.

Overall, the company seems to be keeping a general plan. The company has almost no debt, but it does sell shares to raise capital. The number of shares has more than tripled in the last couple of years, but some of this is due to the conversion of preferred shares in 2020.

Growth and the Future

The DevOps industry is a novel one, and even Jfrog realizes this in their own annual report, and there are not clear patterns yet, like with the autoindustry. This makes growth trends difficult to anticipate.

A limited-functionality version of JFrog Artifactory is licensed under an open source license, which could negatively affect our ability to monetize our products and protect our intellectual property rights.

This is from their 10K’s Risk Factors. It suggests that, while their product is good, it may not have a moat if free riders arise. Even so, its operating cash flows are positive, and it’s growing, which indicates that its customers (some of which are big names) see value and will likely continue to see it.

It’s just unclear if share dilution and the cash devoted to capex will be worthwhile.

Valuation

Given cash spent on investments and depressing effects it has on free cash flow, I will not attempt a valuation.

Growth Assumptions: N/A

Intrinsic Value Per Share: $N/A

Done reading this article? Return to the main library.