INTT: inTest Corporation Stock Research

INTT: inTest Corporation Stock Research

Updated 5/9/2022

Don’t understand some business words here? Open the FAQ in another tab.

Summary of Operations

InTEST Corporation is company whose products allow manufacturers to perform product tests during the manufacturing process. Many of these assist in the development of semiconductors, but they have recently broadened their scope to other industries that can utilize similar testing products, such as thermal tests where a product must prove it can handle extremely high or extremely low temperatures. Their products are typically sold to distributors who then sell them to specific manufacturers, which often include the automobile, aerospace, medical, telecommunications, and others.

About half of revenues come from the “Semi Market,” while the other half come from the “Multimarket” (non-semiconductor). In 2021, the company produced about $11 million in operating cash flows and had about $1 million in additions to property, plant, and equipment. Expenses tend to be concentrated in the first quarter, so annual financials are perhaps the best way to track the company’s performance.

Strategy

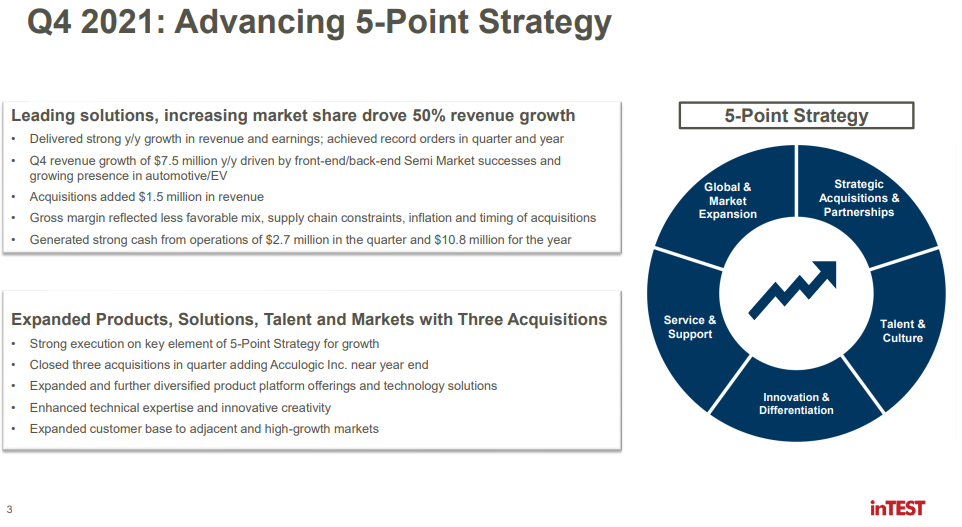

In order to avoid the cyclicality of the semiconductor market, inTEST has focused heavily on expanding into other markets in order to diversify their product portfolio and expand their customer base. While it does commit to organic growth, it mostly acquires other companies whose products will complement its current operations and can be optimized by management. Recently, it took a small loan to help acquire Acculogic in December 2021 (a $8.5 million purchase).

Growth and the Future

The company has a history of successfully optimizing and integrating its acquisitions. Given that it is small, its acquisitions are likely also immature and thus have room for improvement and strong returns on investments. While they are riding the high demand for semis, the future of inTEST is in the multimarket. Battery tests for the rising EV market in the automobile industry are a new frontier for growth as well.

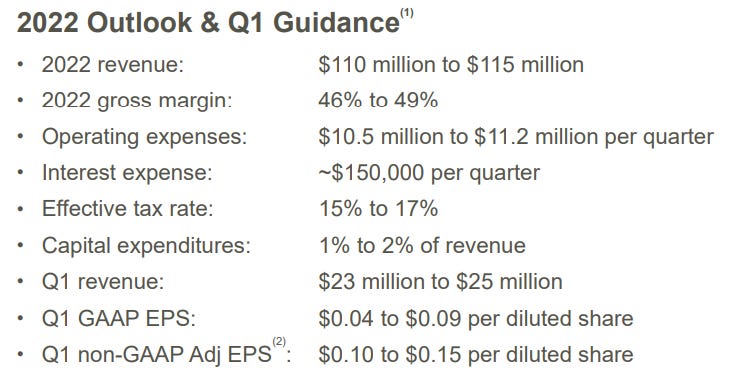

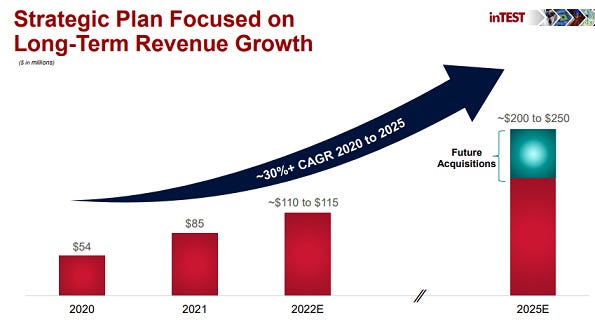

What’s interesting is this company’s guidance for 2022. A reminder: they made about $11 million in operating cash flows in 2021. That’s historically on the high end for them. What could 2022 free cash flow therefore be after these acquisitions? Just take their projected revenue, and then subtract opex, interest expense, taxes, and capex. Should look like (in millions): 110 - 44.8 - 0.6 - 11.08 - 2.3 = $51.22 million. That’s half the current market cap (as of 3/7/2022). Of course, we know they will make more acquisitions, so that needs to be substracted when they happen. Let’s assume they can do $20 million in FCF.

As of Q1 2022, revenues are showing signs of increases from the recent acquisitions. Management intends to make at least one acquisition per year. Even the analyst in the latest earnings call agreed that inTEST gets good prices for its acquisitions.

Valuation

Growth Assumptions: 5%

Intrinsic Value Per Share: $19

Even if it can only do about $10 million in FCF, that just means INTT is fairly valued for a 10% return.

Done reading this article? Return to the main library.