OMF: OneMain Holdings Stock Research

OMF: OneMain Holdings Stock Research

Updated 3/26/2022

Don’t understand some business words here? Open the FAQ in another tab.

Summary of Operations

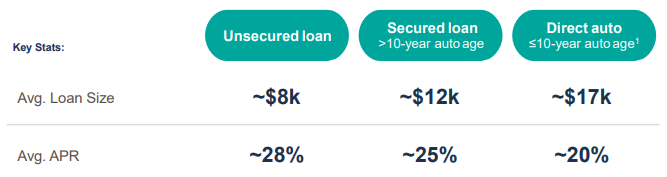

OneMain is a lending company the originates, underwrites, and services personal loans for nonprime customers. It also offers two credit cards, BrightWay and BrightWay+, through a banking partner, and sells insurance policies. They have about 2.4 million accounts across 1,400 locations in 44 states, complemented by their online operations.

Loans typically range 3 to 6 years and have fixed rates. Since their customers are typically higher risk, they tend to charge higher interest rates. The company has a very high dividend yield for something that is not a REIT or a BDC, which appears to be related to these high rates.

Despite their pool of customers, delinquency on loans is not common, and OneMain is able to pivot their staff from originations to collections during stressed times.

Strategy

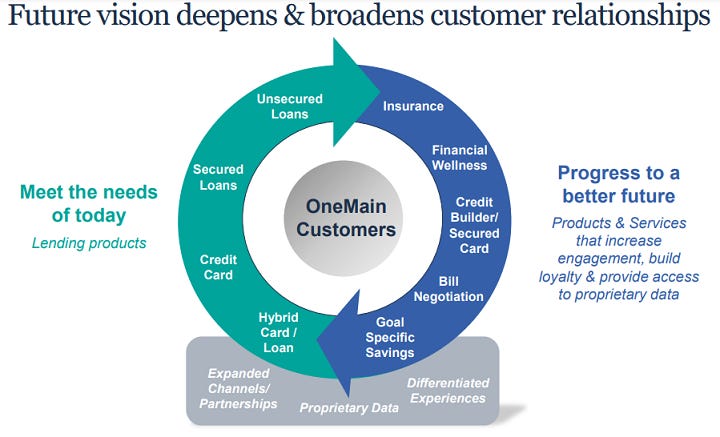

The company believes that its balance between physical and digital services makes it widely accessible, assisted by data analytics that enable the origination of profitable loans. From there, it wants to expand its product offering in order to multiply the dollars per customer it receives.

Growth and the Future

The company has a buyback program, which should grow a holder’s position, but with so much of the country already covered continued growth of the business itself will require it to generate more earnings with its credit card, insurance, and other financial services.

The risk factors mentioned that increasing interest rates could hurt them, given their fixed rate loans. With hyperinflation going on and the Fed primed to make increases, the holder should beware. Growing the product line, like its new credit cards, however, can mitigate this.

Valuation

Given the uncertainty on interest rates and the impact on their ability to grow organically, I think this can only be valued for the dividend for now.

Growth Assumptions: 10% first 5 years; 5% second five

Intrinsic Value Per Share: $47

Done reading this article? Return to the main library.