PFLT: Deep Dive

Don’t understand some business words here? Open the FAQ in another tab.

Description of Business

PennantPark Floating Rate Capital Ltd (PFLT) is Business Development Company (BDC) and Regulated Investment Company (RIC) that provides capital to privately owned, middle-market companies primarily in the form of loans. PFLT has traditionally defined the “middle market” as companies with between $10 million and $50 million of EBITDA. As an RIC, it pays most of its earnings to shareholders through a monthly dividend, at a stable $1.14 per year, in order to avoid federal income tax.

Managed by PennantPark Investment Advisers LLC, PFLT (as a publicly traded company) is an investment vehicle for the capital allocation of the LLC.

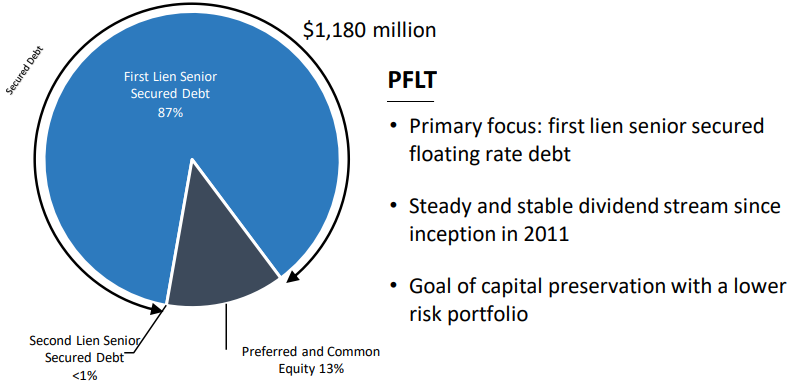

Key Assets

For a current breakdown of its investment portfolio, you can see its filing with the SEC here. There are a lot of companies there, and they are all privately owned, so it’s not practical for us to analyze those, business for business. Nevertheless, we can glean some general insights about this portfolio.

As seen above, PFLT typically maintains its focus on first lien secured debt. To the rookie investor, this means their investments are mostly loans, and the profit they make will be on the interest payments of those loans. Being first lien, it has priority over other types of loans in repayment, in case that company has a bad year and trouble repaying all of its loans to all of its different lenders. This means that our principal as potential owners of PFLT is safe.

The company engages in detailed analyses and discussion with its borrowers. In addition to due diligence on the financials, they negotiate strong covenants to increase the security of the loans. Moving on…

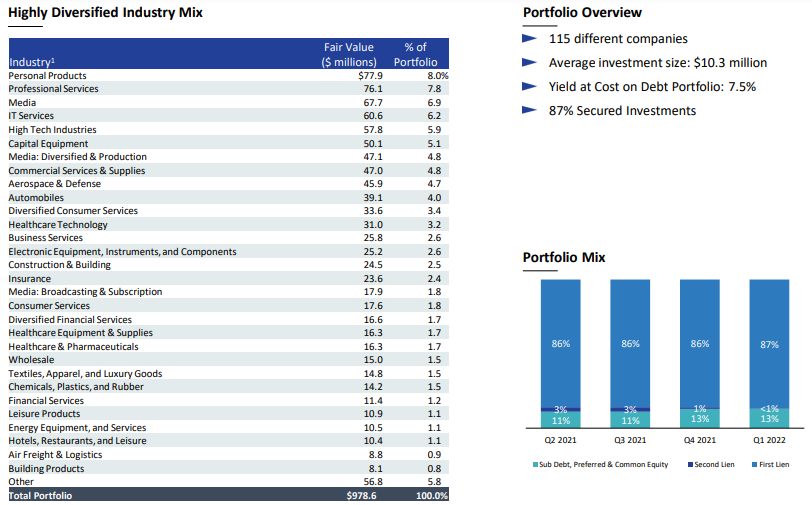

The portfolio is highly diversified into different industries. These also tend to be non-cyclical and have steady cash flows in most macroeconomic scenarios. Consequently, non-accrual rate, even in the pit of the COVID Recession, was negligible, and PFLT did not have to cut or suspend its dividend.

Since 2018, over 75% of their loans are with repeat customers, indicating that not only are steady interest payments to be found in this portfolio, but so are relationships that will lead to future loan originations.

It’s worth noting that about 13% of the portfolio is in equity positions. This is one area where PFLT benefits from capital appreciation (as the portfolio company rises from $10 million to $50 million in EBITDA). These positions are sold after satisfactory growth, usually with a return of 2.9x.

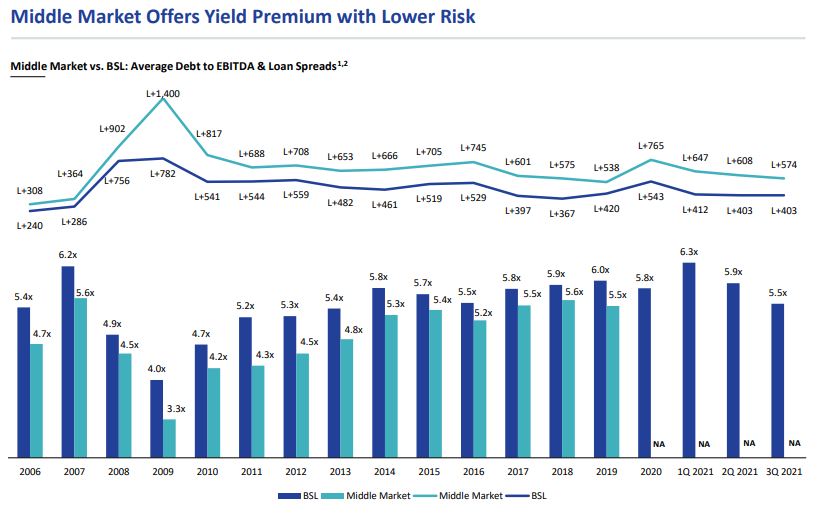

Lastly, if we examine the middle-market nature of the portfolio, the company believes its lower average indebtedness as a class of a businesses makes it lower risk in terms of repayment, while offering superior yields for that level of safety (when compared to loans in general).

In Summary

The assets of PFLT are mostly loans

The borrowing companies are healthy and likely to repay

The interest provides a steady dividend to shareholders

Long-term relationships come from these loans

Capital appreciation comes from equity positions

Financials

The company has about $746 million in debt. The assets, valued around $1.2 billion, more than exceed that. Overall, net asset value per share is positive at $12.70. Much of this debt is long-term and matures in 2026 to 2031. Overall, the company is financially healthy.

With interest being the primary source of income, some will note from the table above that interest income for 2021 fell below 2020 and 2019 levels. This is largely because the COVID crash slowed down origination of new loans in 2020. 2021, by comparison had much higher levels of origination due the backed up demand for capital from the prior year. As such, this is a temporary blip, and 2021’s new loans should materialize in heightened interest income in the coming years, to balance things out.

Also worth nothing is that expenses mainly come from interest on their own loans and fees to the management team (the LLC).

History of the Company

The first seeds were planted in 2007, with the formation of the LLC and the publicly traded PennantPark Investment Corporation (PNNT) by Art Penn. After the Great Recession, Penn saw demand for capital from stressed companies and founded PFLT in 2011. As the only friendly hand to the middle market for the decade after that rough period, PFLT faced little competition and steadily grew its team and relationships with portfolio companies.

PFLT’s key difference from its sister, PNNT, is its narrower, strict focus on first lien secured loans (perhaps reflecting post-recessionary caution). PNNT, by comparison, is mixed with first lien, second lien, unsecured debt, and a much larger share of equity positions. The performance of these portfolios is intriguing, as PFLT’s dividend has been stable, while PNNT has had cut their dividend and still yields lower on price.

Because it is an RIC, very little of the company’s earnings are retained for reinvestment, and PFLT raises capital through taking on its own debt or selling new shares. While the company has been growing over the last eleven years, this growth has been proportionate to share dilution, so the dividend remains consistent but does not grow.

Management Team

Art Penn

Art Penn is the founder of PennantPark (all related enterprises), as well as PFLT’s CEO and chairman. After working in finance and investing from 1992 to 2007, Penn noticed the opportunity of providing loans to the underserved middle market. He has spent the last 15 years building a team of investors in line with his vision. Additionally, he has built deep relationships with companies and individuals in this market. A self-described value investor, his businesses originate loans as if quoting Graham and Dodd directly, seeking safety of principal and sufficient earnings for payment of interest.

PennantPark Investment Advisers

Most of the other team members have more limited information, but they all have tried resumes in investments.

Intrinsic Value

Dividend

The main takeaway from everything I’ve discussed so far is that the company has a solid portfolio and can pay a reliable dividend of $1.14. While it is safe from decline, dilution and the bond-like nature of earnings means that the dividend does not grow. The price is also usually about ten times the value of the dividend, so with 0% growth and valued on that annual $1.14, the intrinsic value should be $8.70.

The price is rarely that low, the 2020 COVID Crash being the only major aberration. Such an opportunity may only arise once per decade, so let’s analyze what happened with this one.

Art Penn bought about $250,000 worth of PFLT during the crash. The dividend yield was over 20% at the time, which alone would have been a powerful return. As we can see, the stock price rebounded in a year, giving him a return of about 3.4x, which is extremely good for just one year. Accomplishing that consistently for a decade would produce a return over 206,000x! A person starting with $1,000 would be a multi-millionaire on that alone.

Now, PFLT is probably not going to offer 3.4x plays every year for ten years straight, but getting a 3.4x return just once can be major. Let’s look at this chart below to see why.

If you take any one of those ten years and make its return 3.4x instead of 10%, you can see the significant difference it has on end results. Thus, the lack of growth makes PFLT a bad holding for a long period of time, but its fundamentals can make for a great short-term play to mighty, single-year multiple on an investment, as happened for Penn himself.

If folks are not sure what to do with money in their portfolio as they readjust positions, the high, monthly yield makes PFLT a reasonable destination. The main risk here is short-term price declines for when an investor decides to redeploy it.