THO: Thor Industries Stock Research

THO: Thor Industries Stock Research

Updated 2/14/2022

Don’t understand some business words here? Open the FAQ in another tab.

Summary of Operations

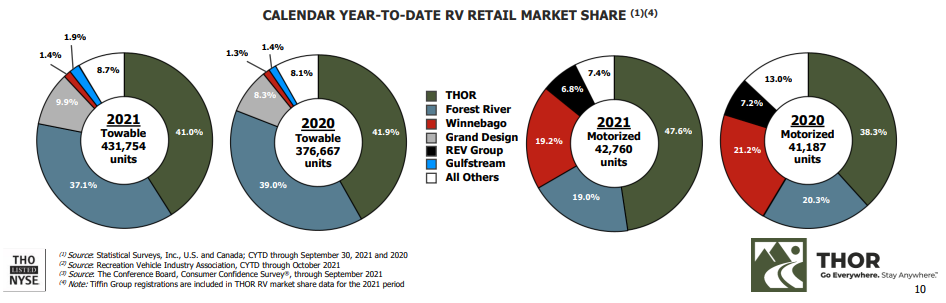

Thor Industries is the largest manufacturer of recreational vehicles (RVs) in the world, mainly through subsidiaries that they have acquired (many of which were in the last few years). It records the operations of its businesses under three segments; North American Motorized (21% of revenues), North American Towable (50%), and European (26%). “Other” operations account for the last 3%, and they mainly sell parts.

Despite having so many subsidiaries, their approach to them is very hands-off, preferring to let the management work out their own relationships with suppliers, dealers, and employees. Subsidiaries even continue to compete amongst themselves. The nature and purpose of these acquisitions, therefore, is a curiosity.

The balance sheet is decent but somewhat leveraged. Operating cash flows have grown about 16% per year over the last decade. Much of this is continually reinvested into new PPE or further acquisitions.

Strategy

Like automobiles in general, RVs are a cyclical and seasonal industry. Factories are typically designed with the ability to increase and reduce productivity in response to demand with flexibility and without much incurred cost.

Nevertheless, the strategy of this company is the sum of the strategies of its subsidiaries. Thor is not stating any vision of leveraging its size and scale. This is strange, considering the concerns it’s expressed in its risk factors (see annual report) about both suppliers and dealers continuing to consolidate, potentially putting Thor in a vice that could depress its margins.

The company seems like an investment mogul whose specialty is the RV industry. That’s not bad per se, but returns will depend on the acquisitions being at low cost relative to the earning power of the asset.

One proactive thing I can see is that their website has a handy interface to match you with an RV product out of their many subsidiaries, based on a handy Q&A feature. They also acquired a supplier called Airxcel in the last quarter, which they hope will meet supply needs, but it’s unclear how much they will continue to acquire with such integration in mind, given their decentralized model.

Growth and the Future

Much of the company’s growth has therefore been enabled by horizontal acquisitions over the past decade. With the current market share that it has, there are not many more opportunities for consistent growth by this method.

Growth would then depend on an organic rise of the RV market. When you think it about it, there is no way this market should be anywhere close to the one for normal cars. RVs are more akin to luxury items and have narrower uses. Where it is similar is in its cyclicality, but COVID had caused a recent and anticyclical spike in demand for RVs, as customers find these products are generally a safer way to travel or have vacations, which the recent regime of lockdowns and social distancing have made difficult or worrisome.

It’s then a question of if this results in a paradigm shift, where these new customers continue to buy and use RVs well after the pandemic after developing a fondness for them. Otherwise, revenues will plateau or crash in the near future as quickly as they ballooned. Conservative growth assumptions are warranted.

Valuation

Growth Assumptions: 7% first 5 years, 0% second 5

Intrinsic Value Per Share: $36

Done reading this article? Return to the main library.