WIRE: Encore Wire Stock Research

Updated 4/20/2022

Don’t understand some business words here? Open the FAQ in another tab.

Summary of Operations

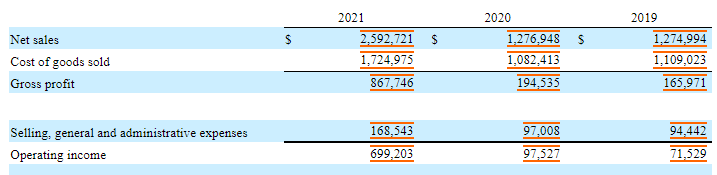

Encore produces electrical wire and cable for buildings. Its main customers are distributors who mostly buy through representatives of independent manufacturers. Most of their operations are in a single location in Texas. The company has an operating margin of 27%.

Strategy

The company believes its vertical, compact structure is low-cost and, with this, that they can expand by leveraging their customer service (speed of order fill) and expanding the scope of their wire products. Its SmartColor ID products allow different wires to be easily identified by those using them. The company uses its own cash and has no debt.

Their main competitors are: Southwire Company, Cerro Wire LLC, General Cable (a company of the Prysmian Group) and AFC Cable Systems, Inc.

Growth and the Future

Copper is a major component of their costs, so the cost of copper and their ability to raise prices if this increases will be key. The wire industry is cyclical for reasons like this, but it does tend to track with the construction industry as well. Biden’s infrastructure bill could therefore mean a boost to cash flows. Alex Ponte from Seeking Alpha notes that the company has a higher return on capital than its peers, which is a good sign as well. There’s a lot going for this company.

Valuation

While 2021 was a great year, let’s assume at least $200 million in free cash flow.

Growth Assumptions: 15% first 5 years; 10% second 5

Intrinsic Value Per Share: $145

Done reading this article? Return to the main library.

Good find. Bought 1, put in a limit buy for 5 more at 105.